Understanding Cigarette Taxes in the EU: Why They're So High

Cigarette smokers across Europe are increasingly aware of the heavy burden imposed by excise taxes on tobacco products. Not only do these taxes significantly inflate the retail price of cigarettes, but they often exceed the cost of the cigarettes themselves. According to the EU Tobacco Tax Directive, each Member State must impose a minimum excise tax on cigarettes, which comprises two components: specific ad quantum taxes and ad valorem taxes based on the retail price.

The Current Landscape of Excise Taxes in 2025

In 2025, the minimum excise tax within the EU remains at €1.80 ($2.12) per pack of 20 cigarettes, adhering to standards that have not been updated since 2014. Additionally, all Member States must ensure that the total excise duty equates to at least 60% of the national weighted average retail price. However, some nations opt for a specific rate higher than €2.30 per pack, exempting them from the 60% rule, leading to diverse tax structures.

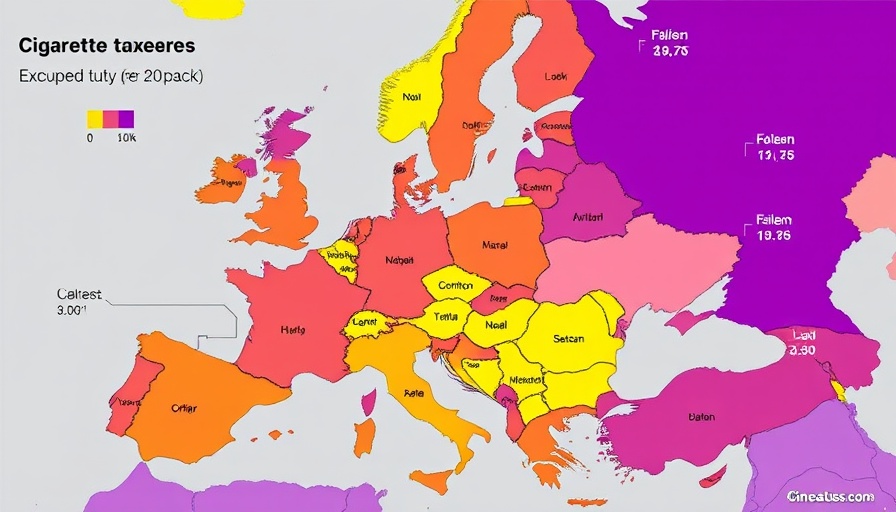

Diversity Across Member States: A Closer Look

A noticeable disparity exists in cigarette excise tax rates across EU nations. For instance, Ireland imposes the steepest tax at €10.71 ($12.64) per pack, making it the most expensive place for smokers. Following closely are France and the Netherlands, with respective taxes of €8.09 ($9.55) and €7.77 ($9.17). This stark contrast, juxtaposed with Bulgaria, which levies scant taxes of just €2.03 ($2.39), highlights the variance in governmental approaches to tobacco regulation.

How Excise Taxes Affect Small to Medium Businesses

For small and medium businesses, particularly those in the tobacco industry or selling consumer goods, understanding these tax frameworks is crucial. Tax burden affects pricing strategies, consumer behaviour, and ultimately the bottom line. Higher taxes may deter customers, forcing businesses to adapt their marketing approaches or reconsider product offerings. Furthermore, compliance with various tax rules across different EU countries can complicate operational logistics, particularly for those engaged in cross-border trade.

Future Predictions: What Changes May Come?

As the EU prepares to update the Tobacco Tax Directive, the landscape of cigarette taxation may shift significantly. Experts anticipate potential increases in minimum tax rates as a part of broader health initiatives aimed at reducing smoking rates. Businesses should brace for these adjustments and consider proactive strategies to cope with potential consumer backlash against price increases.

Counterarguments: The Debate on Tobacco Taxation

While many argue that high cigarette taxes discourage smoking, thus enhancing public health, opponents point to the economic implications of such policies. Some sectors argue that excessive taxation can lead to a black market for tobacco products, circumventing government revenue and safety regulations. Finding a balance between discouraging harmful habits and supporting legitimate businesses remains a contentious point of discussion.

Conclusion: Mindful Decisions for Business Planning

As these dynamics unfold, CPAs and small to medium businesses operating within or alongside these tax frameworks must remain informed and adaptable. Understanding the intricacies of excise taxes in the EU can position these businesses to navigate the implications effectively. The landscape of tobacco taxation is likely to evolve—strategizing in advance can mitigate adverse effects and capitalize on opportunities.

Stay informed about the potential changes in tobacco tax regulations across the EU. Educating yourself on upcoming adjustments enables businesses to make informed decisions that can affect pricing, consumer engagement, and overall operations.

Write A Comment