Understanding Cigarette Smuggling: A Growing Economic Concern

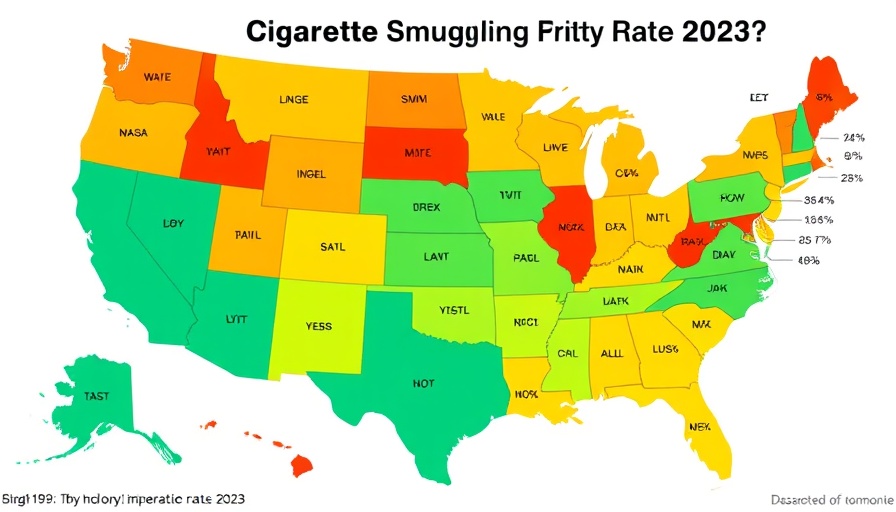

The interplay between cigarette taxes and smuggling has become an alarming economic issue in the United States, especially as tax rates continue to climb. In 2023, California has overtaken New York as the state with the highest rate of cigarette smuggling, with astonishing estimates indicating that over half of the cigarettes consumed in California were not purchased legally. This trend indicates a major factor where tax policies inadvertently fuel black-market activities, leading to substantial revenue losses for states.

The Link Between Tax Rates and Smuggling

As taxes on cigarettes rise, consumers and suppliers alike are drawn to explore alternatives to avoid these heightened costs. The data from 2023 corroborates the strong positive correlation between increased tax rates and cigarette smuggling activities across the nation. With California’s smuggling rate pegged at 52.5 percent and New York closely trailing at 51.8 percent, these figures reflect a growing crisis that challenges traditional market dynamics.

Why Smuggling Thrives: The Economic Drivers

The geographical positioning of states plays a significant role in smuggling behavior. States like Wyoming and Virginia, which have low tax rates, attract smokers from neighboring states where prices are markedly higher due to tax rates. For instance, Wyoming’s smuggling rate is alarmingly high at 55.0 percent, showcasing how consumers engage in cross-border shopping to evade local taxes. This not only benefits smuggled goods but also undermines legitimate businesses striving to comply with tax regulations.

Counterarguments: Perspectives on Taxation

While higher cigarette taxes are seen as a public health initiative aimed at reducing smoking rates, the economic implications reveal a nuanced situation. Some argue that increased taxes could discourage smoking, but the reality is that they may also inadvertently bolster illegal trade. Critics highlight that taxing harmful products isn’t a one-size-fits-all solution; instead, it could pave the way for extensive smuggling networks that weaken the intended public health outcomes.

The Way Forward: Addressing The Smuggling Epidemic

For policymakers, the challenge lies in crafting legislation that balances tax revenue generation with the risk of escalating smuggling activities. Possible solutions include establishing a minimum price for cigarettes or implementing stricter penalties for those caught smuggling. By understanding how smuggling operates, lawmakers can design policies that reduce the appeal of illegal markets while still achieving public health objectives.

Businesses, particularly those operating within the tobacco industry, must also adapt. This means reassessing pricing strategies and enhancing compliance measures concerning taxation. In an era where consumer habits shift rapidly, being agile and informed can help traditional businesses weather the storm created by illicit markets.

Final Thoughts: Recognizing the Economic Landscape

The landscape of cigarette taxation and smuggling reveals a critical intersection of public health and economic policy. As we approach a future where tax rates on cigarettes continue to evolve, understanding the underlying economics becomes essential, not just for policymakers but also for small to medium businesses operating within this sector. By staying informed, businesses can strategize effectively to sustain their operations amidst a turbulent market.

In closing, as this smuggling trend poses a complex challenge, both economic implications and social responsibilities will play a vital role in shaping future discussions around taxation policies. For those involved in the CPA or small business sectors, knowing these dynamics is crucial for navigating compliance and maintaining a competitive edge.

Write A Comment